Walking back to your rental car only to find a sea of shattered glass on the pavement is a traveler’s nightmare. Unfortunately, in major U.S. hubs like San Francisco (where "bipping" is a daily occurrence), Los Angeles, and Seattle, smash-and-grab thefts have reached epidemic levels.

Most travelers panic—not just because of the theft, but because they are terrified of the impending financial fallout. Will the rental company charge thousands? Will my own insurance premiums skyrocket? This guide breaks down the exact steps to take, the complex hierarchy of insurance coverage, and how to use your credit card benefits to save your wallet.

1. First 30 Minutes: What To Do Immediately

The initial discovery of vehicle damage can be overwhelming, but your actions in the following minutes are critical for both your safety and your future insurance claims. Stay calm and follow this prioritized checklist to ensure you are protected legally and financially.

1.1 Make Sure It’s Safe Before Anything Else

-

Assess the Area: If you find the car while the theft is in progress or the area feels sketchy, do not approach. Thieves often operate in crews and can be armed.

-

Do Not Confront: Your safety is worth more than a laptop. Move to a well-lit, populated area before calling for help.

1.2 Should You Call 911 or File a Non-Emergency Report?

-

Call 911 IF: The crime is in progress, there is an immediate threat, or the suspect is still on the scene.

-

File a Non-Emergency/Online Report IF: You discovered the damage after the fact and there are no suspects. In cities like SF or LA, police rarely dispatch officers for a broken window. You will likely be directed to an online portal to file a "cold" report.

1.3 Take Photos of Everything (Inside and Outside the Car)

Before moving the vehicle or cleaning the glass, document the scene:

-

Exterior: Wide shots showing the car's location and close-ups of the broken window/pried locks.

-

Interior: Show the glove box left open, empty seats where bags were, and the glass distribution.

-

Time Stamps: Ensure your phone’s GPS/Time stamp metadata is active. These photos are your primary evidence for insurance adjusters.

1.4 Can You Drive the Car With a Broken Window?

-

Temporary Fix: If the rental agency is far, you can carefully brush out loose glass (use gloves!) and drive.

-

Safety First: If it’s raining or highway speeds are required, visibility and noise may make it unsafe. You have the right to request a tow through the rental company’s roadside assistance, though fees may apply initially.

2. Do You Need a Police Report for Rental Car Damage?

Short answer: YES. A police report is the single most important document in your recovery process. It acts as the official legal record that the damage was caused by a criminal act (vandalism/theft) rather than your own negligent driving.

2.1 Why It Is Non-Negotiable

-

Rental Company Requirement: To process a Damage Incident Report (DCR) as a non-collision event, agencies like Hertz, Enterprise, or Avis almost always require a case number. Without it, they may default to charging you for "negligence" or "unauthorized use."

-

Credit Card Claims: This is the #1 reason claims are denied. Benefit administrators (like Visa or Amex) require a police report filed within 24 to 48 hours to validate that you are a victim of a crime.

-

Personal Property Claims: If you plan to use Homeowners or Renters insurance to recover the cost of stolen items (laptop, bags), they will not even open a file without an official report.

2.2 What If the Police Refuse to Respond?

In many high-crime U.S. cities, police will not dispatch an officer for "property damage only." Do not be discouraged.

-

Online Reporting: Most major cities (e.g., San Francisco's SFPD, LAPD) have an online portal for "Citizen Accounting Reports."

-

Case Number vs. Full Report: You don't need the final typed report immediately. The Temporary Case Number or the confirmation email generated by the online system is usually enough to swap your car at the rental counter.

-

Documentation of Refusal: If you call the non-emergency line and they tell you they won't come, note the time and the dispatcher’s ID if possible.

3.3 Tips for Filing an Accurate Report

-

Be Specific: Mention that "the window was smashed and items were taken from the interior."

-

Include the VIN/License Plate: Make sure the rental car's specific identifiers are in the report so there is no confusion about which vehicle was involved.

-

The 48-Hour Rule: Regardless of how busy you are, file the report within 48 hours. Waiting longer can look suspicious to insurance adjusters and may void your credit card benefits.

3. Vehicle Damage vs. Personal Property Theft — What’s Covered?

It is crucial to understand that Rental Car Insurance and Credit Card Coverage ONLY cover the car itself, not your belongings inside it.

|

Scenario |

Covered by Credit Card / Rental CDW? |

Covered by Homeowners/Renters Insurance? |

|---|---|---|

|

Broken Window / Door Frame |

YES |

No |

|

Entire Vehicle Stolen |

YES |

No |

|

Laptop / Camera Stolen |

NO |

YES (Subject to deductible) |

|

Luggage / Passport / Cash |

NO |

YES (Cash usually excluded) |

4. Contacting the Rental Company

Once the scene is documented and the authorities are notified, you must contact the rental agency to arrange for a vehicle exchange or repair. Navigating this interaction correctly is key to minimizing immediate out-of-pocket costs and avoiding "failure to report" penalties.

4.1 Roadside Assistance vs. Counter

Call the Roadside Assistance number provided in your rental agreement immediately. They will dictate whether you should drive the car to a local branch or wait for a tow.

4.2 Will They Charge You Immediately?

Usually, yes. Upon returning a damaged car, the rental agency will often charge your credit card for the estimated repair cost (or your deductible) on the spot. Don't panic; this is standard procedure. You will use these receipts to get reimbursed by your insurance/credit card.

4.3 How Replacement Vehicles Work

If they have inventory, they will swap you into a new car. Note: Your original rental agreement may be closed and a new one opened. Ensure the damage on the first car is clearly noted as "theft/vandalism" so you aren't blamed for "negligence."

4.4 What is a Damage Incident Report (DCR)?

This is the internal document the rental company creates. Ask for a copy before leaving the lot.

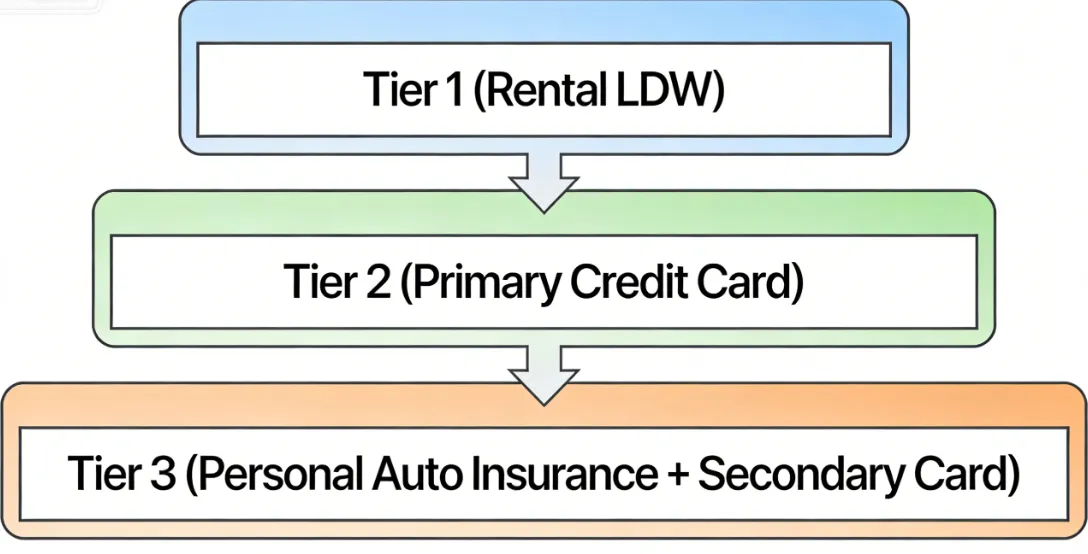

5. Who Pays? Understanding the Insurance "Order of Operations"

This is where most travelers get confused. Understanding the "hierarchy of payment" determines whether you pay $0 or $5,000 out of pocket.

5.1 Rental Company LDW/CDW vs. Credit Card Coverage — What’s the Difference?

What LDW/CDW Actually Is (Damage Waiver, Not Insurance)

Loss Damage Waiver (LDW) or Collision Damage Waiver (CDW) is not technically insurance. It is a contractual agreement where the rental company waives its right to charge you for damage to the vehicle. If you buy this, you "walk away" from the damage without involving any other insurers.

-

Pros: Zero paperwork, no impact on personal insurance, "walk away" convenience.

-

Cons: Expensive ($30–$60/day).

How Credit Card Rental Coverage Works

Most travel credit cards provide an Auto Rental Collision Damage Waiver (ARCDW) as a benefit. This is a reimbursement-based benefit. The card company doesn't prevent the rental agency from charging you; instead, they pay you back for those charges after you file a successful claim.

-

Pros: Free (included with your card).

-

Cons: Requires extensive documentation, you usually pay the rental company upfront and get reimbursed later, and coverage depends on whether it is "Primary" or "Secondary."

Upfront Charges vs. Reimbursement Model

The biggest difference is the immediate financial impact. With Rental LDW, you usually pay nothing at the counter. With credit card coverage, the rental company will charge your card for the repairs (or your deductible) immediately. You must then wait weeks or months for the credit card provider to reimburse you.

Which Option Is Lower Risk?

Rental LDW is the lowest risk but highest cost ($30–$60/day). Credit card coverage is "free" but carries a high administrative burden and requires you to float the repair cost on your own line of credit while the claim is pending.

|

Feature |

Credit Card Coverage |

|

|---|---|---|

|

Upfront charge after damage |

Usually no |

Usually yes |

|

Claim process required |

No |

Yes |

|

Affects personal insurance |

No |

Secondary may |

|

Daily cost |

High ($30-$60) |

Usually included with card |

5.2 Insurance Order Explained — Primary vs. Secondary Coverage

If you choose to use your credit card's coverage, you must know if it is Primary or Secondary.

What Primary Coverage Means

-

First in line: You do not have to notify or file a claim with your personal auto insurance.

-

No personal auto insurance involvement: This protects your personal premium from increasing. It covers the entire theft/damage amount up to the policy limit.

-

Top-Tier Card Examples: The most famous cards offering built-in Primary coverage are the Chase Sapphire Preferred (CSP) (Decline the rental company's collision insurance and charge the entire rental cost to your card. Coverage is primary and provides reimbursement up to $60,000 for theft and collision damage for most rental vehicles with an MSRP of $125,000 or less) and the Chase Sapphire Reserve (CSR) (Decline the rental company's collision insurance and charge the entire rental cost to your card. Coverage is primary and provides reimbursement up to $75,000 for theft and collision damage for most rental vehicles in the U.S. and abroad.)

-

Amex Premium Car Rental Protection: While standard American Express cards offer Secondary coverage, you can enroll in their "Premium" protection. For a flat fee (approx. $12–$25 per rental period, not per day), your coverage is upgraded to Primary. This is a highly recommended "hack" for Amex cardholders.

What Secondary Coverage Means

-

Personal auto insurance first: You must file a claim with your own car insurance (State Farm, Geico, etc.) first.

-

Deductible applies: The credit card only pays for the portion your personal insurance doesn't cover (usually just your deductible).

-

Potential premium increase: Because you filed a claim with your personal insurer, your rates may go up.

Primary vs. Secondary Credit Card Rental Coverage Comparison

| Comparison Dimension | Primary Credit Card (e.g., CSP / CSR) | Secondary Credit Card |

|---|---|---|

| Claim Order (Insurance Priority) | ⭐⭐⭐⭐⭐Acts as the first line of coverage. No need to involve your personal auto insurance. | ⭐⭐You must file with your personal auto insurance first. The credit card only covers remaining eligible costs. |

| Must You File With Personal Auto Insurance? | ❌ No | ✅ Yes |

| Impact on Personal Insurance Premium | ⭐⭐⭐⭐⭐Typically no impact since your personal insurer is not involved. | ⭐⭐Possible premium increase due to recorded claim with your insurer. |

| Claim Complexity | ⭐⭐⭐⭐Straightforward if required documents are provided. | ⭐⭐More complex due to coordination with personal insurance. |

| Overall Risk Control | ⭐⭐⭐⭐⭐Ideal for travelers without U.S. auto insurance or those wanting to protect their premium. | ⭐⭐More suitable for those with stable, comprehensive personal auto insurance coverage. |

*Note: Amex cards are secondary by default but offer a "Premium Car Rental Protection" for a flat fee per rental that makes it Primary.

5.3 Mandatory Prerequisites for Credit Card Claims

To activate your credit card's insurance, you must meet these three conditions:

-

Decline the Rental Company’s CDW/LDW: If you accept their coverage, your credit card coverage is automatically voided in most cases.

-

Pay with the Specific Card: The entire rental transaction must be charged to the card providing the benefit.

-

Primary Driver Name: The person listed on the rental agreement must be the cardholder.

5.4 How the "Order" Works in Real Life

A. If Your Credit Card Offers Primary Coverage

-

Eligible Cards: Chase Sapphire Preferred, Chase Sapphire Reserve, Capital One Venture X.

-

The Workflow: There is no need to involve your personal auto insurance.

-

The Claim: Once the window is smashed, you pay the rental company for the repair. You then file a claim directly with the card’s benefit administrator. They will reimburse you for the full amount (including administrative fees and loss of use) without your personal insurer ever knowing.

B. If Your Credit Card Coverage Is Secondary

-

Eligible Cards: Most standard Visa Signature or Mastercards.

-

The Workflow: You must file a claim with your personal auto insurance first.

-

Deductible Issue: Your personal insurance pays for the window, but you are stuck with the deductible (e.g., $500). Your credit card then kicks in to reimburse that $500 deductible.

-

Premium Impact: Because you filed with your personal insurance, there is a risk of a premium rate hike, even for a comprehensive claim.

C. If You Purchased LDW/CDW From the Rental Company

-

The Workflow: You are typically 100% covered through the rental agency.

-

The Claim: When you return the damaged vehicle, you simply fill out their internal incident report and hand over the keys. There is no claim filed with your personal insurance, and no money typically leaves your pocket at the counter.

D. If You Declined All Coverage

-

Worst-Case Scenario: You are personally and financially responsible for all damages. The rental company will charge your credit card for the full repair, administrative fees, and "Loss of Use." If you don't have personal insurance that covers rentals, this money comes straight out of your bank account.

6. Will This Increase My Personal Auto Insurance Premium?

A smashed window is often the point where travelers hesitate: "Is it worth the risk of my rates going up for years?" Here is how U.S. insurers typically handle these incidents.

6.1 Comprehensive vs. Collision Claims

-

Comprehensive: This covers events out of your control—vandalism, theft, fire, or natural disasters. A smashed window falls under this category.

-

Collision: This covers "at-fault" or "not-at-fault" accidents involving other vehicles or objects.

-

Typical Deductible: Most U.S. policies have a Comprehensive Deductible ranging from $100 to $500. Since a window replacement often costs between $250 and $600, your personal insurance might only pay a small fraction after the deductible is met.

6.2 How Insurers View Rental Car Claims

If you use your personal insurance for a rental car smash:

-

"Not-At-Fault" Status: Insurers generally view vandalism as a "not-at-fault" event. Unlike an accident where you were speeding,破窗盗窃 doesn't reflect your driving risk.

-

The Record: The claim will appear on your CLUE report (Comprehensive Loss Underwriting Exchange), which all major insurers share.

6.3 When Rates Typically Increase

-

The Threshold: Most insurers will not raise your premium for a single comprehensive claim, especially if it's under a certain dollar amount (e.g., $1,000).

-

Multiple Claims: Rates typically increase if you file two or more claims within a 3-year window. If you recently filed a claim for a cracked windshield or hail damage on your own car, adding a rental car smash could trigger a rate hike.

-

State Laws: Some states (like California) have laws that prohibit insurers from raising premiums for "not-at-fault" comprehensive claims.

7. Step-by-Step Credit Card Claim Process

Navigating the credit card claim portal can be tedious. Success depends on following a strict timeline and providing airtight documentation.

7.1 Essential Documents for Credit Card Reimbursement

To ensure your claim isn't stuck in "Pending" for months, upload these 5 essential documents immediately:

-

Copy of the Rental Agreement (Initial & Final): Showing you declined their insurance.

-

Police Report: Or the official Case Number/Online Report confirmation.

-

Damage Incident Report (DCR): From the rental agency.

-

Itemized Repair Estimate/Invoice: Showing exactly how much the window cost.

-

Fleet Utilization Log: (Critical for "Loss of Use" claims) Proving the company actually lost money while the car was in the shop.

-

Credit Card Statement: Showing the rental charge.

-

Photos of the Damage: As taken at the scene.

7.2 Claim Timeline (What to Expect)

-

Day 1–2: Report the damage to the rental company and file the police report.

-

Day 3–45: Call your credit card’s benefit administrator to "Open a Claim." You don't need all documents yet, just a claim number.

-

Day 45–90: The rental company sends you the final bill. Upload all invoices and logs to the card portal.

-

Day 90–120: Typical 2–4 weeks processing starts once the file is "Complete."

-

What delays claims: Missing "Fleet Utilization Logs" (proving Loss of Use) or "Itemized Repair Estimates" are the #1 causes of 3+ month delays.

7.3 Common Reasons Claims Get Denied

-

Accepting Rental CDW: If you paid for the rental company's insurance, the card's benefit is void.

-

Late Filing: Most cards require the claim to be opened within 20–60 days of the incident.

-

Ineligible Vehicle Type: Many cards exclude high-end luxury cars, large vans (10+ passengers), or off-road vehicles.

-

Missing Police Report: Without a formal report filed within 48 hours, the claim is almost always denied as "unverifiable."

8. Hidden Fees: The "Unexpected Charges"

Hidden Fees

Rental companies don't just charge for the glass. They may add:

-

Administrative Fee: $50–$150 just for "processing" the paperwork.

-

Loss of Use: Charges for every day the car is in the shop and cannot be rented to others.

-

Diminished Value: The drop in the car's resale value because it now has a "damage history."

-

Towing: If the car was undrivable.

、

、

Common Mistakes That Can Cost You Thousands

-

Not Documenting the Interior: If you don't show the glass inside, they might argue the window was broken from the inside (your fault).

-

Missing the Deadline: Most credit cards require you to initiate a claim within 20–60 days. If you wait for the final bill to arrive in the mail (which can take months), you might be too late.

-

Admitting Liability: Never say "It was my fault for parking there." Simply state the facts: "I parked at X time, returned at Y time, and found the window smashed."

11. FAQ

Q: Does a smashed window count as a "collision"?

A: No. In the insurance world, vandalism and theft are classified as "Comprehensive" claims, not collision claims.

Q: What if I used credit card points or "Free Night" vouchers to pay for the rental?

A: Most premium cards (like Chase Sapphire) provide coverage as long as at least a portion of the rental was charged to the card, or if you used points earned directly from that card's program to book the trip.

Q: Will my credit card cover the damage if I split the payment across two different cards?

A: Usually, no. Most credit card benefit policies require the entire rental transaction to be charged to the specific card providing the coverage to remain eligible.

Q: The rental company is offering me a replacement car. Will the insurance continue?

A: Yes, but ensure the rental agency closes the old agreement and starts a new one (or updates the existing one) with the new VIN. Verify that the damage to the first car is clearly documented as "Theft/Vandalism" so it doesn't carry over to your new agreement.

Q: I only have "Secondary" coverage on my card, and I don't have personal car insurance. What happens?

A: Good news: In this specific case, "Secondary" coverage usually becomes "Primary." If you can prove you do not have an active personal auto policy, the credit card will pay from dollar one.

Q: Does credit card insurance cover "glass only" damage without a full theft?

A: Yes. Whether the thieves took your bags or just broke the glass and left, the physical damage to the vehicle is covered under the Collision Damage Waiver (CDW) benefit.

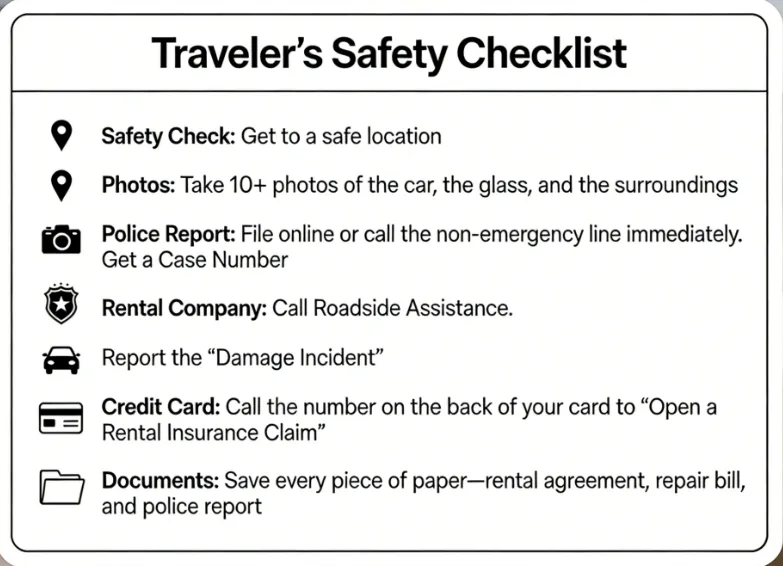

12. Final Checklist (Printable Summary)

-

Safety Check: Get to a safe location.

-

Photos: Take 10+ photos of the car, the glass, and the surroundings.

-

Police Report: File online or call the non-emergency line immediately. Get a Case Number.

-

Rental Company: Call Roadside Assistance. Report the "Damage Incident."

-

Credit Card: Call the number on the back of your card to "Open a Rental Insurance Claim."

-

Documents: Save every piece of paper—rental agreement, repair bill, and police report.

Disclaimer: This guide is for informational purposes. Insurance terms vary by provider. Always check your specific Credit Card Guide to Benefits and Personal Auto Insurance Policy.