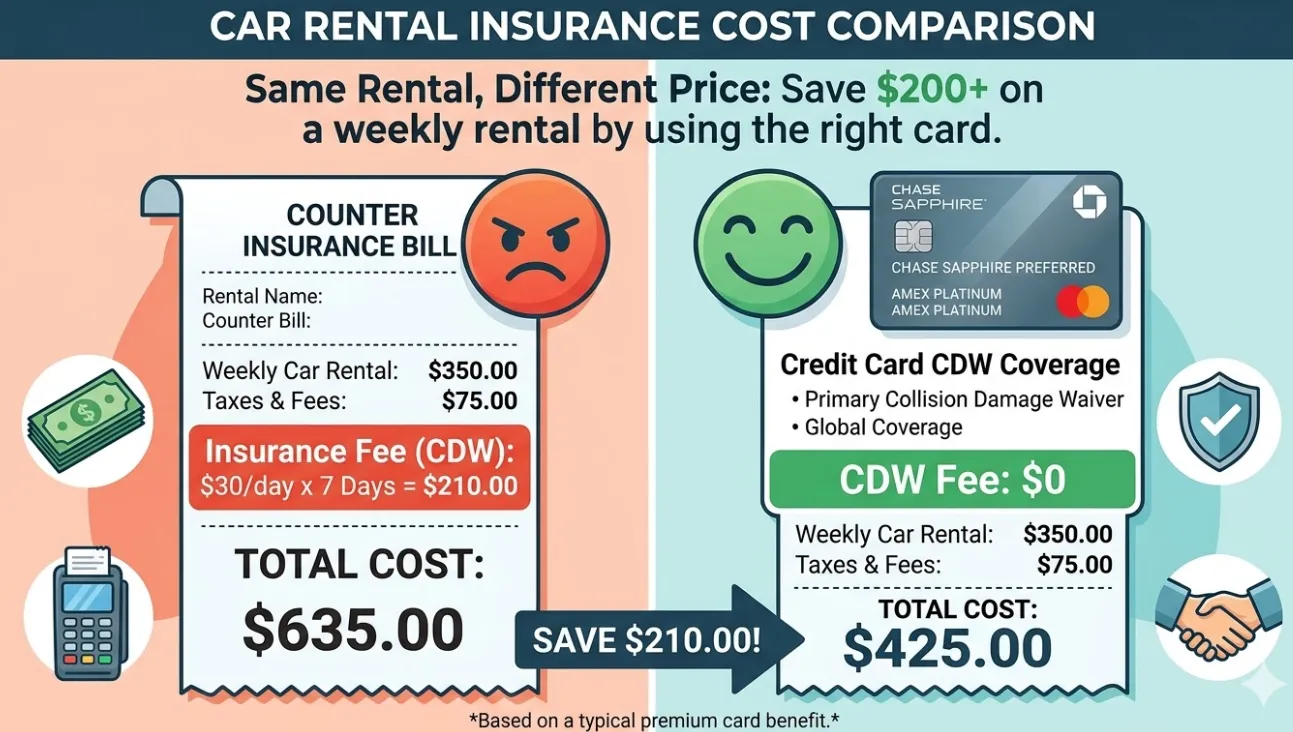

When planning a road trip, we spend hours hunting for flight deals and hotel upgrades, only to get hit with a $30/day insurance fee at the rental counter. In 2026, those fees can easily double your rental cost.

The secret? The "Key" to free insurance is already in your wallet. Most premium credit cards offer built-in Auto Rental Collision Damage Waivers (CDW). Here is how to unlock this benefit and save hundreds on your next trip.

In this guide, you’ll learn:

-

What CDW/LDW actually is

-

How credit card rental insurance works

-

The difference between primary and secondary coverage

-

The best credit cards for rental insurance

-

How to use it correctly (and avoid costly mistakes)

1. What Is Car Rental Insurance?

Types of Rental Car Insurance

Rental companies promote three main types of coverage. You need to know which ones your card handles:

-

CDW/LDW (Collision/Loss Damage Waiver): This covers damage to the rental car or theft of the vehicle. This is what your credit card covers.

-

Liability Insurance (LIS/TPL): This covers damage to other people’s property or medical bills for others. Most credit cards DO NOT cover this.

-

Personal Effects Coverage (PEC): Covers your luggage/laptop. Usually covered by your homeowners or renters insurance.

What Does CDW Actually Cover?

Before relying on your card, you must understand the scope of the "Waiver." It is generally split into covered incidents and strict exclusions:

Covered:

-

Collision damage: Physical damage to the rental vehicle caused by an accident or weather.

-

Theft of the vehicle: Total loss of the car due to theft or damage caused during an attempted theft.

-

Towing charges: Reasonable costs to tow the vehicle to the nearest repair shop following a covered accident.

NOT Covered (The Deal-Breakers):

-

Driving under the influence: Any drugs or alcohol in your system voids the coverage immediately.

-

Off-road driving: Driving on unpaved roads (gravel, sand, trails) is a breach of contract and is not covered.

-

Unauthorized drivers: Only drivers listed on the rental agreement are protected.

-

Tires & Windshield (sometimes): Many cards consider "road hazard" damage (like a rock chipping the glass or a nail in the tire) as maintenance rather than a collision.

Why Is CDW So Expensive?

You might wonder why a simple waiver costs almost as much as the car rental itself. Here’s the reality:

-

High Profit Margin: CDW is a massive profit center for rental agencies. Because they self-insure their fleets, the "daily fee" you pay is mostly pure profit once the statistical risk is covered.

-

Daily Pricing Model: Unlike annual personal insurance, CDW is sold by the day. This makes the effective annual rate astronomical—often exceeding several thousand percent of the vehicle's value.

-

Lack of Transparency: Counter agents often use "fear-based" selling, focusing on the worst-case scenario while keeping the actual low cost of fleet maintenance hidden from the consumer.

An illustration of a rental car:

Green Checkmarks (Covered by Card): Dents, scratches, broken windows, theft, towing.

Red X Marks (NOT Covered by Card): Other driver's injuries, damage to other cars, stolen laptop inside the car.

⚠️ The "California Trap": The Liability Black Hole

This is the most dangerous pitfall for travelers.

In certain states like California, rental companies are NOT legally required to provide even a minimum amount of third-party liability insurance.

-

If you have personal auto insurance: Your policy usually follows you to the rental.

-

If you DON'T have US auto insurance (e.g., International tourists, NYC residents without cars): You are driving completely uninsured for third-party damages. If you hit a luxury car or injure someone, you could face millions in lawsuits.

-

Pro Tip: In this specific case, you MUST purchase the LIS (Liability Insurance Supplement) or SLI at the counter. It’s expensive, but it protects your life savings.

⚡ The 2026 EV Alert: Tesla & Rivian Risks

In 2026, you are highly likely to be assigned an Electric Vehicle (EV). This brings new insurance risks:

-

Extreme Repair Costs: The repair cost for EVs—especially if the battery pack is damaged—is significantly higher than gas cars. A minor underbody scrape can result in a total loss claim.

-

The Coverage Gap: Many "Secondary" cards have lower payout limits (e.g., $25k–$50k) which may NOT cover the full replacement cost of a Rivian R1S or a Tesla Model X.

-

Why Primary is Mandatory: Premium cards like the Chase Sapphire Reserve (CSR) offer a $75,000 limit, which is essential for covering high-tech EV components. Always verify your card's MSRP limit before driving off in a luxury EV.

2. 💳 How Credit Card Rental Insurance Works

Many premium credit cards offer CDW coverage for free when you meet three specific requirements:

-

Pay for the rental with the card: The entire transaction must be charged to the card providing the benefit.

-

Decline the rental company’s CDW: You must explicitly say "no" to the rental agency's own collision coverage.

-

Are listed as the primary driver: The name on the credit card must match the primary name on the rental agreement.

Why Do Credit Cards Offer This?

-

Provided by Networks: These benefits are usually negotiated by card networks like Visa, Mastercard, and American Express.

-

Encourage Card Usage: By providing high-value travel protections, banks encourage you to use their card for large travel purchases, which generates transaction fees and increases customer loyalty.

Rental Company Insurance vs. Credit Card Insurance

Before choosing your card's coverage, understand the operational difference between the two:

|

Feature |

Rental Company CDW |

Credit Card CDW |

|---|---|---|

|

Cost |

$20–$40 per day |

FREE (Included in annual fee) |

|

Deductible |

Usually $0 |

Varies (Paid by card issuer) |

|

Claim Process |

"Walk away" convenience |

You must file a claim & provide paperwork |

|

Impact |

No impact on personal insurance |

None (if Primary); High (if Secondary) |

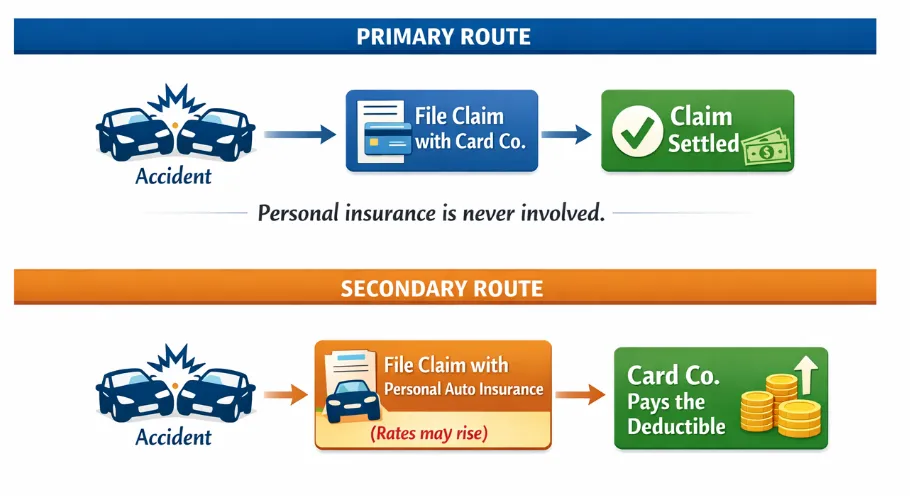

3. ⚖️ Primary vs Secondary Coverage

This is the most critical distinction in the credit card world:

Primary Coverage (The Gold Standard)

-

How it works: If you crash, the card company pays first.

-

The Benefit: You don't have to notify your personal auto insurance. Your personal premiums will not increase.

-

Top Cards: Chase Sapphire Reserve, Chase Sapphire Preferred, Capital One Venture X.

Secondary Coverage

-

How it works: You must file a claim with your personal insurance first. The card only pays your deductible and leftover costs.

-

The Downside: Your personal insurance rates might go up after the claim.

-

Top Cards: Amex Platinum (unless you pay for the "Premium" upgrade), most Visa Signature cards.

Primary vs. Secondary Credit Card Rental Coverage Comparison

| Comparison Dimension | Primary Credit Card (e.g., CSP / CSR) | Secondary Credit Card |

|---|---|---|

| Claim Order (Insurance Priority) | ⭐⭐⭐⭐⭐Acts as the first line of coverage. No need to involve your personal auto insurance. | ⭐⭐You must file with your personal auto insurance first. The credit card only covers remaining eligible costs. |

| Must You File With Personal Auto Insurance? | ❌ No | ✅ Yes |

| Impact on Personal Insurance Premium | ⭐⭐⭐⭐⭐Typically no impact since your personal insurer is not involved. | ⭐⭐Possible premium increase due to recorded claim with your insurer. |

| Claim Complexity | ⭐⭐⭐⭐Straightforward if required documents are provided. | ⭐⭐More complex due to coordination with personal insurance. |

| Overall Risk Control | ⭐⭐⭐⭐⭐Ideal for travelers without U.S. auto insurance or those wanting to protect their premium. | ⭐⭐More suitable for those with stable, comprehensive personal auto insurance coverage. |

Which One Should You Choose?

|

Situation |

Recommendation |

|---|---|

|

Frequent renter |

Primary (Best protection for your rates) |

|

No personal auto insurance |

Primary (Simplified claim process) |

|

Occasional renter |

Secondary is OK (Enough for low-risk use) |

4. 🏆 Best Credit Cards for Rental Car Insurance (2026)

Choosing the right card depends on your travel frequency and budget. While some cards carry high annual fees, the "Primary" insurance benefit alone can offset that cost in just one or two week-long trips.

How to Choose the Right Credit Card

Before picking a card, evaluate these three pillars of your travel profile:

-

Based on Your Travel Habits:

-

Travel often: Go for a Premium card (e.g., Chase Sapphire Reserve). The annual credits and high coverage limits ($75k+) are designed for heavy users.

-

Rare rentals: A Basic card with secondary coverage (like the Bilt Mastercard) is usually enough to cover your deductible if something goes wrong.

-

-

Based on Your Insurance Situation:

-

No personal car insurance: You MUST choose a card with Primary coverage. Since you have no other policy, even a "secondary" card would technically become primary, but true Primary cards have much smoother claims departments.

-

Already insured: Secondary coverage may suffice, but remember that your personal premiums could spike if you have to file a claim through your main provider first.

-

-

International Travel Considerations:

-

Country Exclusions: Always check if your destination is excluded (Italy, Australia, and New Zealand are common problem areas for some issuers).

-

Coverage Limits: Ensure the "Actual Cash Value" or the specific limit ($50k or $75k) covers the cost of a rental car in the country you are visiting.

-

Top Card Contenders for 2026

|

Card Name |

Coverage Type |

Annual Fee |

Max Limit |

Why we love it |

|---|---|---|---|---|

|

Primary |

$795 |

$75,000 |

The industry standard; covers "Loss of Use" and administrative fees. |

|

|

Primary |

$395 |

$75,000 |

Includes Hertz President's Circle status and a $300 travel credit. |

|

|

Primary |

$95 |

Up To $60,000 |

The best "budget" way to get Primary insurance for under $100. |

|

|

Secondary |

$695 |

$75,000 |

Can be upgraded to Primary for a flat $12–$25 per rental. |

|

|

Primary |

$350 |

Up To $60,000 |

A great airline card option that doesn't skimp on Primary CDW. |

|

|

Secondary |

$0 |

$50,000 |

The only $0 annual fee card that offers solid rental protection |

5. ✅ How to Use Credit Card CDW (Step-by-Step)

To successfully trigger your credit card's insurance, you must follow these steps in precise order. A single missed detail could void your coverage entirely.

Step 1: Verify Your Card’s Policy

Before booking, call the number on the back of your card to confirm your specific CDW benefits. Ask for a "Letter of Coverage" to be emailed to you; this is essential for international rentals.

Step 2: Pay the Entire Bill with the Right Card

Use the card that provides the benefit to book and pay for the full rental amount. Avoid using "points + cash" or split payments unless your card issuer explicitly permits it.

Step 3: Ensure the Names Match

The primary driver listed on the rental agreement must be the cardholder. If a spouse or friend is the primary driver but you pay with your card, the insurance will likely be denied.

Step 4: Explicitly Decline the Rental Company’s CDW/LDW

At the counter or on the website, you must check the box that says "Decline Collision Damage Waiver". If you accept their coverage, your credit card insurance becomes invalid.

Step 5: Perform a Thorough Pre-Drive Inspection

Take a high-quality video walking 360-degrees around the car. Document every scratch, dent, and wheel scuff. This is your defense against "pre-existing" damage claims.

6. 🚨What to Do If You Have an Accident

Even the most careful drivers face unexpected incidents. If you are involved in a collision or discover damage to your rental vehicle, follow this protocol to ensure your credit card claim is successful.

Immediate Steps

-

Ensure Safety First: Pull over to a safe location, turn on hazard lights, and check for injuries. Call emergency services (911 in the U.S.) if anyone is hurt.

-

Call Authorities: In many jurisdictions, a Police Report is mandatory for insurance claims, especially if a third party is involved or the damage is significant.

-

Document Everything (Take Photos): Before moving the vehicles (if safe), take high-resolution photos of the damage to both cars, the license plates, and the overall scene (street signs, weather conditions).

Notify Required Parties

-

Rental Company: Call the roadside assistance or emergency number provided in your rental packet immediately.

-

Credit Card Benefits Administrator: You must open a "Claim" as soon as possible.

-

👉 Timeline: Most issuers require notification within 24–48 hours of the incident. Delaying this can lead to a denial based on "late reporting."

-

Note: You don't need all the paperwork yet; you just need to establish the case number.

-

Documents You’ll Need for the Claim

To get reimbursed, you will eventually need to upload the following digital copies:

-

Rental Agreement: The initial contract showing you declined their CDW.

-

Incident/Damage Report: The internal report generated by the rental agency.

-

Repair Estimate: A detailed breakdown of the costs to fix the vehicle.

-

Credit Card Statement: Proving you paid for the rental with the specific card.

-

Police Report: Highly recommended (and often required) for major claims.

7. Critical Warnings (The "Fine Print")

-

The Turo Trap: Most credit card insurance does not cover Turo. If you use peer-to-peer car sharing, you usually need to buy the platform's insurance.

-

Excluded Countries: Standard exclusions often include Israel, Jamaica, and the Republic of Ireland. Always request a "Letter of Coverage" from your bank before traveling internationally.

-

The 31-Day Limit: Most cards only cover rentals up to 31 consecutive days.

-

Vehicle Types: Exotic cars (Ferraris), large vans (15+ passengers), and RVs are almost always excluded.

8. Common Mistakes to Avoid

Even with the best card, small errors in judgment or execution can lead to a rejected claim. Watch out for these common "traps":

-

Pitfall 1: Assuming it covers liability ❌

-

The Mistake: Thinking that "Full Coverage" from your credit card means you are protected if you hit another car or person.

-

The Reality: CDW only covers the car you are driving. If you don't have personal auto insurance, you are effectively uninsured for third-party damages.

-

-

Pitfall 2: Using a debit card ❌

-

The Mistake: Using a debit card for the reservation or the final payment.

-

The Reality: Credit card insurance benefits are tied specifically to credit accounts. Debit cards—even those with a Visa or Mastercard logo—almost never include rental car CDW.

-

-

Pitfall 3: Not declining the rental company’s CDW ❌

-

The Mistake: Checking "Yes" for the rental agency's insurance out of fear or confusion.

-

The Reality: Your credit card coverage is "excess" or "supplemental." If you buy the agency's policy, your credit card will refuse to pay, as they assume the other insurance handles it.

-

-

Pitfall 4: Letting someone else drive ❌

-

The Mistake: Letting a friend take the wheel when they aren't on the contract.

-

The Reality: If an unauthorized driver crashes, the insurance is voided. Most cards only cover the cardholder and drivers explicitly listed on the rental agreement.

-

-

Pitfall 5: Renting excluded vehicles ❌

-

The Mistake: Renting a large moving truck (U-Haul) or an exotic sports car.

-

The Reality: Standard credit card policies exclude "specialty" vehicles. Always check the MSRP limit (often $75,000) and vehicle type before assuming you're covered.

-

9. FAQ

Q: What if I don't have personal car insurance?

A: If you have no other insurance, a "Secondary" card automatically becomes "Primary" for you. It covers the full cost of damage up to the card's limit.

Q: Does it cover Tesla or EVs?

A: Most premium cards (like CSR) cover standard EVs like the Tesla Model 3 or Y. However, high-end "Exotic" models (Model X or Cybertruck) may be excluded due to MSRP limits (usually $75,000).

Q: Should I buy Liability (LIS/TPL) at the counter?

A: YES, if you do not have a personal auto policy. Credit cards do NOT cover third-party lawsuits or medical bills for others. Without LIS, you are personally liable for millions in potential damages.

Q: Does the insurance work for Turo or Getaround?

A: Generally, NO. Credit card insurance is designed for "Commercial Rental Agencies" (Hertz, Avis, Enterprise). P2P car-sharing platforms like Turo are usually excluded from the benefit terms.

Q: Is there a deadline to file a claim?

A: YES. You must typically notify the card administrator within 20–45 days and submit all final paperwork within 90 days. Missing these "claim windows" is the #1 reason for valid claims getting denied.

Q: Does it cover "Loss of Use" and "Diminished Value"?

A: Only high-end cards like Chase Sapphire Reserve explicitly cover "Loss of Use" (the money the rental company loses while the car is being fixed). Most basic cards do not, which could leave you with a $500+ bill even after the repair is paid for.

10. Summary: The 2026 Pro-Hacker Checklist

-

[ ] Use a Primary coverage card (CSP/CSR/Venture X).

-

[ ] Decline the CDW/LDW at the counter.

-

[ ] Take photos/video of the car's condition before leaving the lot.

-

[ ] Keep every receipt and the original signed contract.

Drive safe and keep your money in your pocket!