Finding a pile of shattered glass where your car window used to be is a traumatic experience. Take a deep breath. You are safe, and we are going to walk through this step-by-step.

0. Introduction: Who This 2026 Survival Guide Is For (and Who It’s Not)

This guide is specifically designed for:

-

Road-trippers and Renters: Those using rental cars (Hertz, Enterprise, etc.) and relying on credit card insurance.

-

New Residents & Students: International students or expats living in high-risk US metro areas.

-

Credit Card Enthusiasts: Holders of Chase Sapphire Preferred (CSP), Amex Platinum/Gold, or other cards with travel protection.

1. Before It Happens: The Pre-Incident Checklist 90% of Drivers Miss

This section determines whether a break-in becomes a minor inconvenience or a financial nightmare.

High-Risk Environments: Where Break-ins Cluster

In 2026, the "Smash & Grab" epidemic is defined more by the type of location than just the city. Thieves target areas with high turnover and high-value cargo:

-

Tourist-Heavy Areas: Iconic landmarks where drivers are likely to leave luggage while taking photos.

-

Rental Car–Dense Neighborhoods: Areas near airports or transit hubs where "Barcode Stickers" on windows signal a trunk full of travel gear.

-

Outdoor & Scenic Hotspots: Remote trailheads and scenic overlooks where hikers are away from their vehicles for extended periods.

-

Unsecured Urban Parking: Downtown street parking and poorly lit hotel "overflow" lots.

Common High-Risk Examples: San Francisco (e.g., Fisherman's Wharf), Oakland, Los Angeles (e.g., Santa Monica), and Seattle.

The "Bait": Items Most Likely to Trigger a Break-in

Thieves in 2026 operate on a simple, brutal logic: Thieves don’t steal items — they steal possibilities. Even if a bag is empty, a thief sees the possibility of a laptop inside.

-

The Golden Rule: “Hide it” < “Remove it”. Moving a bag to the trunk while parked is often too late; professional thieves watch parking lots for people "hiding" goods. If it stays in the car, it remains a target.

-

Trunks Are Not Vaults: The trunk is not always safe, especially in hatchbacks and SUVs. Modern thieves often smash the small triangular rear window just to "peek" or pull the seat release to see what’s in your cargo area.

-

The "Invisible" Triggers: Visible USB cables, loose coins, sunglasses, or even an empty shopping bag that might look like it contains valuables.

-

High-Value Tech: Laptops, tablets, and cameras. Note that professional thieves often use Bluetooth scanners to detect "sleeping" electronics in trunks.

-

The Suction Mark: The ring left on your windshield by a phone mount signals to thieves that a high-end smartphone or GPS might be hidden in the glovebox.

Insurance Reality Check: What Needs to Be Set Up Beforehand

Before you start your engine, you must verify your coverage logic. Confirm Your Credit Card Covers Break-Ins (Not Just Accidents). Not all rental coverage treats theft, vandalism, or break-ins the same way.

-

Pay the Full Amount: Ensure you use the same card (e.g., CSP or Amex Platinum) to pay for the entire rental transaction. Using partial vouchers or split payments often voids coverage.

-

CDW / LDW Meaning: Collision Damage Waiver (CDW) and Loss Damage Waiver (LDW) are not technically "insurance" but an agreement that the rental company won't hold you liable. If you decline this at the counter to use your card's benefit, you are essentially self-insuring via your bank.

-

Activation Check: For Amex, did you enroll in the "Premium Car Rental Protection"? (This is a per-rental fee service). For Chase, ensure the card is active and in good standing.

-

Coverage Scope: Beforehand, confirm that your card covers:

-

Broken windows

-

Interior damage caused by forced entry

-

Towing or temporary immobilization

-

Some policies emphasize “collision” and bury break-ins under different wording. Knowing this in advance saves hours of frustration later.

Essential Links to Save on Your Phone Right Now

-

Local Police Online Reporting Portal: Search "City Name" File Police Report Online" and bookmark it immediately.

-

Your Auto Insurance App: Ensure apps like GEICO, State Farm, or Progressive are logged in and ready.

-

Credit Card Benefit Dashboard: Bookmark access to Chase (eClaimsLine) or Amex Assurance portals.

2. Right After the Break-In: A Step-by-Step Emergency Workflow

When you discover a car break-in, adrenaline kicks in. What you do in the first 30 minutes often determines whether your claim is approved smoothly — or questioned later.

Follow the steps below in order. Skipping or reordering them can cause unnecessary delays.

Step 1: Immediate Safety and Documentation

-

Do: Take high-resolution photos of the entry point, the "void" where items were, and wide shots of the surrounding context (street signs/landmarks).

-

Don't: Touch anything inside the vehicle or clean up the glass until documentation is complete.

-

Why this matters: Insurance claims rely on "Forced Entry" evidence. Moving items or clearing glass before photographing can lead to claim denial due to "lack of physical proof."

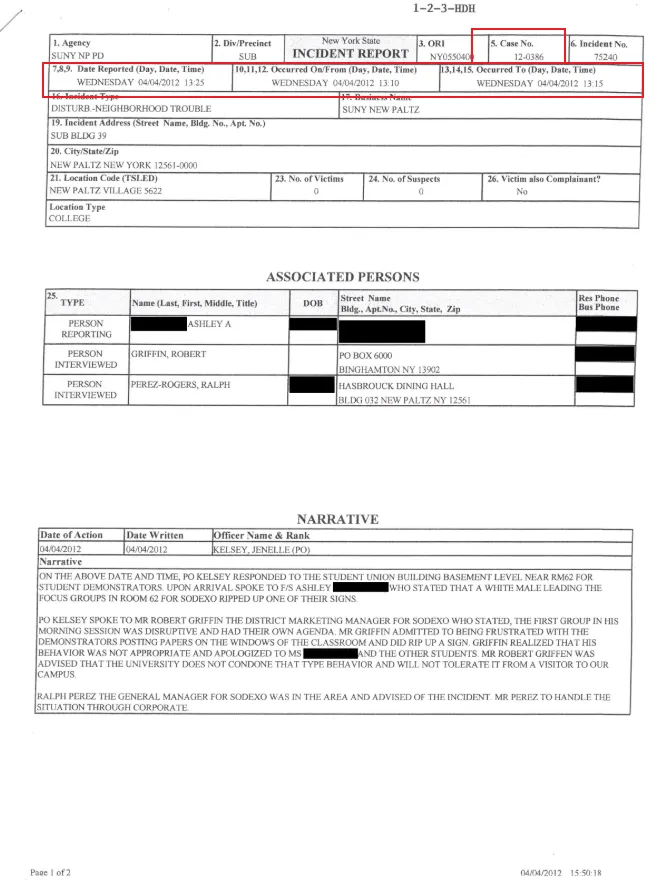

Step 2: The Police Report (T+10–30 min)

-

Do: Use the city’s Online Reporting Portal or non-emergency line; use precise terms like "Forced Entry" and "Theft." Understand the three levels of documentation you will receive:

-

Temporary Case ID: Provided immediately upon online submission. (Useful for swapping rental cars but usually not enough for insurance).

-

Case Number / Incident Number: The permanent reference number assigned once a clerk reviews your report.

-

Official Police Report: The full PDF narrative. This is the only document insurance adjusters will accept as final proof.

-

-

Don't: Call 911 unless the suspect is still on the scene or there is an immediate physical threat.

-

Why this matters: A case number is the "Entry Ticket" for any credit card or insurance claim. Online portals are faster and provide a digital trail that is easier to forward to adjusters.

Step 3: Stakeholder Notification (T+30–60 min)

-

Do: Contact the following parties to secure your claims and vehicle:

-

Rental Company: Report the damage immediately and request a vehicle exchange at the nearest major hub (ideally an airport).

-

Credit Card Benefit Administrator: Call the number on the back of your card to open a "Rental Car Collision Damage Waiver" claim. Ask for the specific deadline for document submission.

-

Personal Auto Insurance: (Required ONLY for your own car or Secondary Card Coverage) For Primary Coverage (like CSP/Amex Premium), do NOT contact your personal insurer. By bypassing them, you ensure this incident never appears on your personal claims history, keeping your future premiums low. Only contact them if your card's coverage is "Secondary" to your personal policy.

-

Secondary insurance means the coverage only applies after a primary insurance policy has been used first. In practice, this means you must file a claim with the primary insurer before the secondary coverage can reimburse any remaining costs, such as deductibles or uncovered fees. If the primary claim is skipped or incomplete, secondary insurance may not pay at all.

-

Don't: Admit fault or say "I think I left the door unlocked" to the rental agency. Simply state the facts of the vandalism. Don't call your personal insurance if you have Primary Card Coverage on a rental—it may cause your premiums to rise unnecessarily.

-

Why this matters: Credit card coverage has strict reporting windows (often 60-90 days). For Secondary coverage, your personal insurance must deny the claim or pay their portion before the card issuer will cover the deductible.

Step 4: Digital and Financial Lockdown

-

Do: Remotely lock/wipe stolen electronics using "Find My" and call your bank to cancel (not just freeze) any stolen physical cards.

-

Don't: Wait to see if the items "turn up." Thieves in 2026 sort and sell high-value tech within the first hour.

-

Why this matters: Reducing the window of opportunity for identity theft or fraudulent charges is as critical as recovering the physical cost of the items.

3. Rental Cars vs. Personal Vehicles: Why the Process Is Very Different

The path to financial recovery depends entirely on the ownership of the vehicle and the type of protection you have active. In 2026, navigating these channels correctly determines whether you pay a $500 deductible or walk away with $0 out-of-pocket costs.

Channel Matrix: Who Pays for What?

It is critical to distinguish between damage to the Vehicle and loss of Personal Belongings. They are almost always handled by different insurers.

|

Scenario |

Liability for Vehicle (Glass/Locks) |

Liability for Belongings (Tech/Bags) |

|---|---|---|

|

Rental Car (Primary Card) |

Credit Card (CSP/Amex Premium) |

Renter’s / Homeowner’s Insurance |

|

Rental Car (Secondary Card) |

Personal Auto Ins. first, then Card |

Renter’s / Homeowner’s Insurance |

|

Owned Vehicle |

Personal Auto Ins. (Comprehensive) |

Renter’s / Homeowner’s Insurance |

Rental Cars: Process-First, Permission-Based

When your rental is hit, your goal is to swap the car as fast as possible while ensuring the paperwork doesn't leave you liable for the full value of the vehicle.

What You Must Do:

-

Head to the Airport: Immediately drive to the nearest Major Airport Hub (e.g., SFO, LAX). Local city branches often lack the authority or inventory to handle damaged swaps. Airport hubs have 24/7 staff and deep inventory.

-

Open a Claim at the Counter: Hand the agent your Police Case Number and the Vehicle Incident Report. Insist on a printed copy of the "Vehicle Damage Report" signed by the agent.

-

Request an Immediate Swap: Since you already paid for a rental period, you are entitled to a replacement vehicle.

Critical Files to Retain (The "Golden Folder"):

-

The Initial Rental Agreement: Proving you declined CDW/LDW.

-

Signed Damage Appraisal: The document generated when you return the broken car.

-

Internal Incident Report: The rental agency's version of the story. The content should be consistent with the Police Report.

-

Final Damage Bill/Demand Letter: Usually mailed 30 days later—this is what you send to your credit card company.

What You Cannot Do Freely:

-

Do NOT Authorize Independent Repairs: Never take a rental car to a local glass shop yourself. This violates your rental contract and will void your credit card insurance coverage.

-

Do NOT Leave Without Paperwork: If the agent says "we'll email it later," stay there. You need a physical or digital receipt showing the car was returned in damaged condition to start your card's claim clock.

-

Do NOT Upgrade Voluntarily: If they offer you a "better" car because yours was broken, clarify if it's a free swap. Accepting a paid upgrade mid-rental can confuse the credit card's "Total Amount Paid" rule.

Even if damage seems minor, acting without approval can shift full liability back to you.

Personal Vehicles: Insurance-Driven, Owner-Controlled

For vehicle owners, the challenge is balancing the speed of repair against the long-term impact on your insurance premiums and the resale value of your car.

What You Must Do:

-

Verify "Comprehensive" Coverage: Ensure you have comprehensive coverage active. Unlike collision, this handles vandalism and "acts of nature."

-

Insist on OEM Glass for Tech-Heavy Cars: If your car has ADAS (Advanced Driver Assistance Systems), rain sensors, or a Head-Up Display (HUD), demand Original Equipment Manufacturer (OEM) glass. Cheap aftermarket glass can cause sensors to fail or display ghost images.

-

Body Shop Selection Strategy: Choose between Insurance-Preferred Shops (Direct Repair Programs) and Independent Shops.

-

Preferred Shops: Faster approval and often a "Life-of-Ownership" warranty guaranteed by the insurer.

-

Independent/Dealer Shops: Better for specialty cars; you have more control over OEM parts usage, but you may have to pay the "labor rate difference" if the shop charges more than the insurer's standard.

-

-

Get a "Not-At-Fault" Letter: Ask your adjuster for a confirmation that this incident is a "non-fault vandalism claim" for your records.

Critical Files to Retain (The "Claims Tracker"):

-

The Itemized Repair Estimate: Showing exactly what parts were used.

-

Proof of Deductible Payment: Often needed for potential reimbursement from secondary card benefits.

-

ADAS Recalibration Certificate: Proof that your car’s cameras and safety systems were re-aligned after the glass was replaced.

-

Detailed Photos of Glass Markings: Capturing the logos/safety stamps on the new glass to ensure it matches the original.

What You Cannot Do Freely:

-

Do NOT Ignore Minor Cracks: Modern car structural integrity relies on the windshield. A small crack from a break-in can lead to airbag failure in a future accident.

-

Do NOT File Small Claims Automatically: If the total repair cost is $\$600$ and your deductible is $\$500$, do NOT file a claim. For the sake of a $\$100$ payout, you lose your "Claim-Free Discount" and increase your risk profile on the CLUE report.

-

Do NOT Settle for Aftermarket "OEE" without Consent: Many shops will install "Original Equipment Equivalent" glass without telling you. It is often thinner and less noise-insulating than true OEM.

Are Stolen Personal Items Covered?

NO. A common misconception is that car insurance covers "everything in the car." It does not.

-

Vehicle Policy: Covers the glass and damage to the dashboard/locks.

-

Belongings: These are covered by your Renter’s or Homeowner’s Insurance. Note that these policies also have deductibles (usually $\$500+$).

-

The Loophole: Check your credit card for Purchase Protection. If the stolen item was bought with that card within the last 90–120 days, the card issuer may reimburse you for the theft, bypassing car insurance entirely.

Side-by-Side Comparison

| Category | Rental Car | Personal Vehicle |

|---|---|---|

| Vehicle ownership | Rental company | You |

| Police report | Almost always required | Sometimes optional |

| Repair authorization | Rental company | You |

| Insurance priority | Credit card often primary | Personal auto first |

| Out-of-pocket risk | Immediate charges possible | Deductible likely |

| Process flexibility | Low | High |

| Timeline | Faster, stricter | Slower, flexible |

The Insurance Agent Checklist: Questions to Ask

-

"Will this vandalism claim count against my 'No-Claims' status?"

-

"Does my policy cover OEM (Original Equipment Manufacturer) glass or just aftermarket?"

-

"If I pay out of pocket, can you still record this as an 'Information Only' report in case I find hidden damage later?"

4. Credit Card Insurance Claims: CSP vs. Amex in the Real World

Credit card rental coverage looks simple on paper. In reality, most claims fail or stall not because of eligibility, but because of documentation, timing, and wording.

This section focuses on how Chase Sapphire Preferred (CSP) and American Express actually behave during a real break-in claim, not how they describe coverage in brochures.

Primary vs. Secondary Coverage: The Financial Impact

If you are renting, the "type" of credit card coverage you have is the single most important factor in protecting your long-term insurance premiums.

-

Primary Coverage (e.g., CSP, Amex Premium):

-

How it works: The card issuer is the first line of defense. They pay the rental company directly for repairs.

-

The Advantage: You do not have to file a claim with your personal insurance. This prevents the break-in from appearing on your CLUE report, ensuring your monthly premiums don't skyrocket.

-

Cost: $0 deductible for you.

-

-

Secondary Coverage (Standard Amex/Visa/Mastercard):

-

How it works: You must first exhaust your personal auto insurance. The credit card only pays what your personal insurance won't (typically just your deductible).

-

The Downside: You must file a claim with your personal insurer. Even if you aren't at fault, this claim remains on your record for 3-5 years and may increase your rates.

-

Cost: You pay your personal deductible upfront, then wait for reimbursement from the card.

-

Essential Conditions for a Valid Claim

-

The "Full Payment" Rule: You must initiate and complete the entire rental transaction with the specific card. If you use a partial voucher or pay the balance with another card, the claim may be voided.

-

The "Decline" Mandate: You must formally Decline the rental agency's Collision Damage Waiver (CDW/LDW). If you accept their insurance, your credit card benefit becomes void as it cannot "double-insure" the same risk.

-

The 31-Day Clock: Coverage typically ends after 31 consecutive days. If your road trip is longer, you must "close" and "re-open" a new rental agreement to reset the clock.

2026 Core Comparison: CSP vs. Amex

Chase Sapphire Preferred (CSP)

American Express Platinum Card

In 2026, the battle for the best travel insurance is fought between Chase (Visa Infinite/Signature) and American Express. While both offer protection, their execution and "hidden" benefits differ significantly.

|

Feature |

Amex (Standard/Secondary) |

||

|---|---|---|---|

|

Type of Coverage |

Primary |

Secondary (Domestic) / Primary (Int'l) |

Primary |

|

Deductible |

$0 |

Depends on personal policy |

$0 |

|

Cost |

Included in Annual Fee |

Included in Annual Fee |

$12.25 - $24.95 per rental |

|

Max Coverage |

Up to $60,000 |

Up to $75,000 |

Up to $100,000 |

|

Loss of Use |

Fully Covered (with Fleet Log) |

Generally Covered |

Fully Covered |

|

Personal Property |

Not Covered (use Homeowners) |

Not Covered |

Up to $5,000 (Secondary) |

Handling "Hidden" Fees from Rental Agencies

Thieves don't just steal your items; the rental company will charge you for the "ghost costs" of the incident.

-

Loss of Use (LOU): This is the daily rate for the car while it sits in the shop. Chase and Amex Premium require a Fleet Utilization Log from the rental company to prove they actually lost money (i.e., they didn't have other cars available).

-

Administrative Fees: These range from $50 to $150 just for "processing" the damage. Both CSP and Amex Premium usually cover these, but only if they are itemized.

-

Towing Charges: Covered up to the nearest qualified repair facility.

The "Golden" Documentation Checklist (2026 Edition)

-

Initial & Final Rental Agreements: Must show your name as the primary driver and the "Decline" of CDW.

-

The "Demand Letter": An official letter from the rental company (e.g., Hertz/Avis) stating the total amount you owe.

-

Incident Photos: Both wide-angle and macro shots of the damage.

-

Final Police Report: Note that a "Case Number" is insufficient; you need the full, finalized PDF narrative.

-

Repair Estimate: An itemized breakdown from the body shop or internal rental maintenance facility.

-

Credit Card Statement: Showing the rental transaction and the charge for the damage.

Claims Portal Mastery

-

Chase (eClaimsLine): Use

eclaimsline.com. It is a third-party administrator (Card Benefit Services).-

Pro-Tip: If they ask for a document you don't have (like a Fleet Log), ask the rental company for their "Loss of Use substantiated documentation."

-

-

Amex Assurance: Log in via the Amex App under "Benefits" > "Claims Center." Amex is known for faster adjudication, often resolving glass claims within 10-15 business days if all photos are uploaded correctly.

What Neither CSP nor Amex Will Cover (100%)

Regardless of card issuer, the following are almost never reimbursed:

-

Personal items stolen from inside the car

-

Indirect losses (missed flights, hotel changes, trip delays)

-

Pre-existing damage or unrelated wear

-

Repairs done without rental company authorization

-

Incidents outside the rental period

If something isn’t part of the vehicle itself, assume it’s not covered unless explicitly stated.

5. After the Report: Warnings, Delays, and Common Pitfalls

Navigating the aftermath requires extreme attention to detail. One missing signature or an incorrectly worded statement can result in a denied claim worth thousands of dollars.

-

The "Case Number" Trap: Do not assume your work is done once the officer hands you a case number. Most 2026 insurance portals require the Full Narrative Report (PDF). It can take 3–10 business days for the police records department to finalize this. Check your email daily for the download link.

-

The "Loss of Use" Dispute: Rental companies (like Hertz or Enterprise) will charge you for the revenue they lost while the car was being repaired. Warning: Chase and Amex will only pay this if the rental company provides a Fleet Utilization Log proving they were at 90%+ capacity. If the rental company refuses, you may be stuck with a $200 - $500 bill.

-

Avoid "Admissions of Negligence": When speaking to the rental company or insurance adjuster, stick to the facts of the entry. Avoid saying phrases like "I was only gone for a minute" or "I might have forgotten to set the alarm." These can be coded as negligence, which is a standard exclusion in many 2026 benefit guides.

-

The "Double Deductible" Hit: If you have personal items stolen AND car damage, you might be facing two separate deductibles: one for your auto insurance (window) and one for your homeowners/renters insurance (stolen laptop). Always calculate if the payout exceeds the combined cost of both deductibles before filing.

-

Sub-Contractor Scams: Be wary of unauthorized towing companies that arrive at the scene before you've called for help. Only use the roadside assistance provided by your rental agreement or credit card to ensure the towing fees are covered.

-

The False Assumption of Automatic Coverage (CSP/Amex): One of the most common reasons for claim denial is the misunderstanding of "automatic" protection.

-

CSP "Full Payment" Requirement: Your Chase Sapphire Preferred insurance will almost certainly be voided if the rental fee is not paid in full with that specific card. If you use a different card for a portion of the payment or even a small rental voucher, the insurance usually becomes invalid.

-

Amex "Premium" Manual Enrollment: Standard Amex cards are Secondary by default in the US. To get Primary coverage, you must manually enroll in "Premium Car Rental Protection" and pay a flat fee per rental (typically $19.95–$24.95). If you don't activate this, you are stuck with the agonizing secondary claim process involving your personal insurance.

-

6. Pro Tips: How to Minimize Risk Next Time (Without Being Paranoid)

Preventing a break-in in 2026 requires a blend of psychology, discipline, and technology. Thieves are more sophisticated, but you can make your vehicle an "unattractive target" through active deterrence.

The "Clean Cabin" Policy (Non-Negotiable)

-

Zero-Visibility Rule: It is not enough to hide bags under seats. In 2026, thieves look for "bulges" or shadows under seat covers. Your cabin must look like it just rolled off the factory floor—no charging cables, no empty coffee cups, and absolutely no shopping bags.

-

The Glovebox & Console Reveal: In high-risk areas like San Francisco, leave your center console and glovebox physically open and empty. This visual confirmation tells a thief that smashing your window will yield zero profit.

-

Wipe the Windshield: If you use a phone mount, the suction cup leave a circular "tell" on the glass. Thieves know this means a high-end smartphone or dashcam is likely in the car. Keep a microfiber cloth handy and wipe the ring off every time you park.

Counter-Tech Strategies

-

The Bluetooth Sniffer Shield: Professional thieves use apps to scan for the Bluetooth/Wi-Fi signals emitted by "sleeping" laptop or tablets. If you must leave a device in the trunk, power it completely off (do not just close the video/sleep mode).

-

Faraday Pouches: For cars with Keyless Entry/Start, store your key fob in a Faraday bag when staying in ground-floor motels. This prevents "Relay Attacks" where thieves amplify your key's signal to unlock the car without breaking the glass.

-

AirTag Hidden Layers: Hide an AirTag inside the car's lining (not just in a bag). While it won't prevent the break-in, it can help police track the "drop-off" point where thieves sort through stolen goods.

Tactical Parking Decisions

-

The "Wheel-to-Curb" Lock: Park in a way that makes the car hard to move, but more importantly, park in "Active" areas. Avoid the corners of parking garages. Instead, park near the elevator or the "Pay Station" where foot traffic is highest.

-

Back-In Parking: If you have a hatchback or SUV, backing into a spot against a wall makes it physically difficult for someone to open the trunk or scan the rear cargo area.

-

The 5-Minute "Quick Stop" Myth: Most break-ins occur within 3 minutes of you leaving the car. Never leave a bag inside "just for a second" to grab a coffee or take a photo at a scenic overlook.

7. FAQ: Real Questions People Ask After a Break-In

Q: Do I still need a police report if nothing was stolen?

A: Yes. Even if nothing is missing, a police report documents the incident officially. Most rental companies and credit card insurers require it to process claims, and vague or missing reports can delay or deny reimbursement.

Q: Can I move or drive the car immediately after a break-in?

A: Only if it’s safe. Take photos first. Check windows, locks, and vehicle drivability. Moving a damaged car without documentation can jeopardize claims or violate rental agreements.

Q: What if I don’t have the police report number when filing a credit card claim?

A: You can notify the insurer that a claim is coming, but most CSP/Amex claims will not be fully processed until you provide an official report number. Early notification protects eligibility, but final approval requires complete documentation.

Q: How does the process differ between rental cars and personal vehicles?

A: Rental cars: The rental company controls repairs and approvals. Credit card insurance is often primary. Police reports are almost always required. Personal vehicles: You control the repair and claim process. Personal auto insurance is typically primary, and credit card coverage is secondary.

Q: Which credit card should I use: CSP or Amex?

A: There’s no universal answer:

-

CSP: Efficient and predictable for clean, well-documented claims.

-

Amex: More flexible for edge cases or imperfect documentation.

The key is knowing documentation requirements before filing.

Q: What items are never covered by credit card insurance?

A:

-

Personal belongings inside the car

-

Indirect losses (missed flights, hotel changes)

-

Pre-existing damage

-

Unauthorized repairs

-

Incidents outside the rental period

If it’s not vehicle damage, assume it’s not reimbursable.

Q: Can I leave the city or state before filing a report or claim?

A: Not recommended. Filing must be done within specific timelines for both police and credit card claims. Leaving before completing reports can result in denials or delays.

Q: What should I save on my phone in case of a break-in?

A:

-

Police non-emergency contact and online report link

-

Rental agreement PDF or screenshots

-

Photos of the car and surroundings

-

Credit card claim portal and login

-

Receipts and proof of payment

Q: What’s the biggest mistake most people make after a break-in?

A: Treating rental cars like personal vehicles and assuming credit card coverage is automatic. Both lead to denials, delays, and frustration. Following the correct workflow — step by step — is what separates smooth claims from chaos.

Disclaimer: This guide is for informational purposes only. Policy terms and conditions are subject to change and should be verified with your provider in 2026.